Archive Collection

Lupot, Gand, Bernardel, Caressa, Français

Reading Support

These archives detail the daily life of great French stringed-instrument makers from 1816 to 1944.

General Ledgers

General ledgers are accounting documents regrouping financial transactions per account (clients, suppliers etc.), as opposed to chronological listing in journals.

General ledgers from the Gand, Bernardel, Caressa and Français collection cover years 1816 to 1923 in a quasi-continuous manner. Only years 1831 to 1839 are missing.

They were completed as needs occurred, and accounts are not in a logical order. One must refer to the directories index to identify all pages or folios

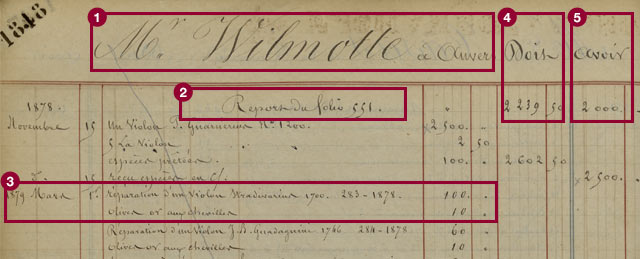

Example of a General Ledger

General ledgers page layout evolves throughout the years, but their structure generally remains similar to the following:

- 1- Account holder

-

« Mr Wilmotte à Anvers »

"Mr Wilmotte in Anvers"

- 2 - Report

-

« Report du folio 551 »

"Report of folio 551"When an account covers several pages, sums previously recorded as debit and credit are carried forward to locate the latest entries.

- 3- Detail of transactions done by or for the account holder

-

« 1879 Mars 1er : réparation d’un violon Stradivarius 1700. 283 – 1878. 100 [F.] / Olives or aux chevilles. 10 [F.] »

"1st March, 1879: repair of a Stradivarius violin 1700. 283 – 1878. 100 [F.] / Gold adornments added to tuning pegs. 10 [F.]"

- 4- Account Debit

-

« Doit : 2 239,50 [F.] »

Due: 2 239.50 [F.]"This column records sums paid in advance by the workshop as well as services or products received by the client and not paid yet.

- 5- Account credit

-

« Avoir : 2 000 [F.] »

"Credit voucher : 2 000 [F.]"The column totals sums paid by the account holder to the workshop.

- Double-Entry Accounting

- Workshop bookkeeping follows double-entry accounting principles.

In this system, operations (purchase, sale, repair etc.) are portrayed as value movements between several accounts – representing the firm’s clients and suppliers, or a value – e.g. goods or cash register. Thus, an instrument purchase is recorded as money transfer between cash register and client accounts.

For each account, movements (received or given value) are recorded in a two-part graph: left, what is received (called "Doit" (due) or "Débit") and right, what is given (called "Avoir" (credit voucher) or "Crédit"). When a client pays for an instrument, the transaction value is recorded as cash register account debit and client credit.

Any value registered as debit on an account incurs credit on another, and if no mistake was made, "debit" and "credit" column totals remain identical within a same document group (journals, account ledgers etc.).

Directories

Directories index the accounts described in general ledgers.

Each listing is linked to a general ledger. It lists accounts alphabetically, indicating relevant page or folio numbers.

Note: Directory/general ledger pairs stand out since their farthest dates are similar. Thus, the directory covering 1912 till 1920 (n° inv. E.981.8.48) will match the general ledger on years 1912 till 1920 (n° inv. E.981.8.47).

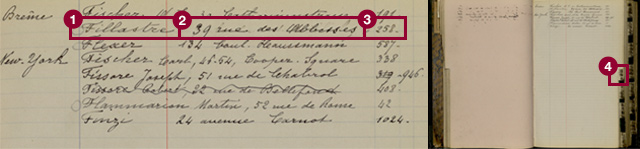

Example of a Directory

- 1 - Account holder name

-

« Fillastre »

- 2 - Account holder address

-

« 39 rue des Abbesses »

- 3 - General ledger page or folio number

-

« 258 »

- 4 - Alphabetical index

-

« Fi »

Journals

Journals are accounting documents listing financial transactions chronologically, contrary to general ledgers regrouping them per account.

The Gand, Bernardel, Caressa and Français Collection counts few journals: only four remain. They concern years 1852-1854, 1920-1944 and 1931-1938. There are two kinds:

- Daily journals

- Monthly journals

Daily Journals

Two journals (n° inv. E.981.8.1 and n° inv. E.981.8.30) list workshop transactions daily.

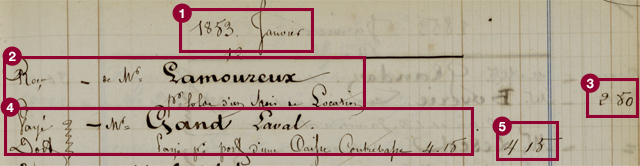

- 1 - Date

-

« 1853 Janvier / 12 »

"1853 January / 12"

- 2 - Transaction detail

-

« Reçu de Mr Lamoureux / pour solde d’un chois (sic) de location »

"Received from Mr Lamoureux / in full payment of a rental choice"

The French sentence records a misspelling, "chois" instead of "choix".

- 3 - Account credit

-

« 2.50 [F.] » The column totals sums paid by the account holder (Mr Lamoureux) to the workshop.

- 4 - Transaction detail

-

« Payé / Doit - M. Gand, [résidant à ] Laval. / Payé pour le port d’une caisse contrebasse : 4,15 [F.] »

"Paid / Due – Mr Gand, [residing in] Laval. Paid for shipping of a double bass case: 4.15 [F.]""Paid" indicates the sum was paid in advance by the workshop.

"Due" indicates the client owes the sum.

- 5 - Account debit

-

« 4,15 [F.] »

This column totals sums paid in advance by the workshop as well as services or products received by the client and non-paid yet.

Monthly Journals

Two – general - journals (n° inv. E.981.5.7 and n° inv. E.981.5.31) only contain monthly and yearly balance sheets. They probably summarize journals specialized per account (client, cash register etc.) which were not recovered.

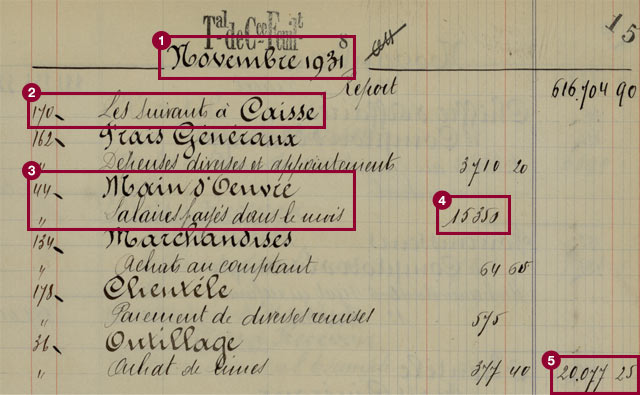

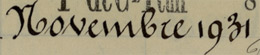

- 1 - Date

-

« Novembre 1931 »

"November 1931"

- 2 - Credited account

-

« 170 » : account number

« Les suivants à Caisse » : "Les suivants à caisse" means the lines that come next indicate a set of transactions between the account they refer to and the cash register account. Taking out "les suivants à" leaves "caisse" aligned on the left, signifying it (the cash register account) was credited during the aforementioned transactions. This means it actually paid the money.".

- 3 - Debited account

-

« 44 » : account number

« Main d’oeuvre » ("skilled workers"): the phrase aligned left indicates this account was debited during transaction. Thus it received the money.

« salaires payés dans le mois » ("Salaries paid in the month"): transaction detail

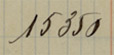

- 4 - Transaction amount

-

« 15 350 [F.] »

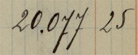

- 5 - Movements total

-

« 20 077,25 [F.] »

This figure totals every transaction, be they receipts or expenses. It was probably used to monitor possible mistakes.

- Double-Entry Accounting

- Workshop bookkeeping follows double-entry accounting principles.

In this system, operations (purchase, sale, repair etc.) are portrayed as value movements between several accounts – representing the firm’s clients and suppliers, or a value – e.g. goods or cash register. Thus, an instrument purchase is recorded as money transfer between cash register and client accounts.

For each account, movements (received or given value) are recorded in a two-part graph: left, what is received (called "Doit" (due) or "Débit") and right, what is given (called "Avoir" (credit voucher) or "Crédit"). When a client pays for an instrument, the transaction value is recorded as cash register account debit and client credit.

Any value registered as debit on an account incurs credit on another, and if no mistake was made, "debit" and "credit" column totals remain identical within a same document group (journals, account ledgers etc.).

Instrument Registers

Some collection registers list instruments made, repaired or examined by workshop luthiers.

Filled over long periods (no less than sixty years for some), registers hold information such as instrument description, owner names and repair overviews. Reading them sheds light on the instrumental landscape back then.

There are four registers:

- Sale of new and old instruments (1840-1902)

- New instruments Inventory (1854-1902)

- Analysis of instruments brought in for repair (1903-1914)

- Finding instrument owners (written in Albert Caressa’s day?)

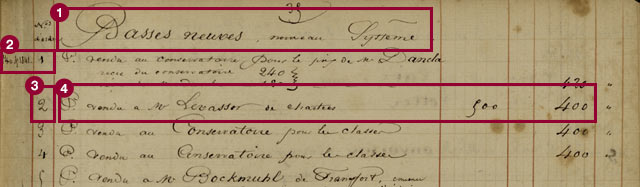

Selling new and old instruments (1840-1902)

This register (n° inv. E.981.8.38) lists old and new instrument sales by the workshop between 1840 and 1902. It provides precious information on instruments made by the workshop: order numbers, construction date, name of first owner, sale price…

- 1 - Instrument type

-

« Basses neuves, nouveau système »

"New basses, new system"

- 2 - Year of making

-

« [1]840 & 1841 »

- 3 - Listing per instrument number

-

« 2 »

- 4 - Buyer’s name and sale price

-

« P. vendu à M. Levasseur de Chartres. 500 [F.] - 400 [F.] »

"P. sold to Mr Levasseur from Chartres. 500 [F.] - 400 [F.]"

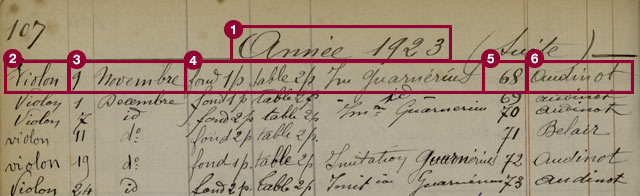

New instrument inventory (1854-1937)

This register (n° inv. E.981.8.8) is a workshop document recording instrument making between 1854 and 1937. Layout slightly evolved over time, but one can generally find the following information:

- 1 - Year of making

-

« Novembre 1931 »

"Year 1923"

- 2 - Instrument type

-

« Violon »

"Violin"« Les suivants à Caisse » : L’expression “les suivants à caisse” indique que les lignes qui vont suivre expriment toutes une transaction entre le compte qu’elles mentionnent et la caisse. Si l’on fait abstraction de l’expression “les suivants à ”, on s’aperçoit que le terme “caisse” est aligné à gauche et qu’il a donc été crédité lors de ces opérations. Ceci signifie que c’est lui qui a versé l’argent.

- 3 - Manufacturing end date

-

« 9 novembre »

- 4 - Instrument description

-

« fond 1 p[ièce], table 2 p[ièces], im[itation] Guarnerius »

"1 piece back, 2 piece table, Guarnerius copy"

- 5 - Order number

-

« 68 »

- 6 - Head manufacturing luthier’s name

-

« Audinot »

Analysis of instruments brought in for repair (1903-1914)

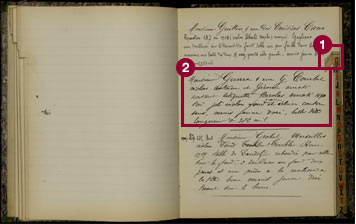

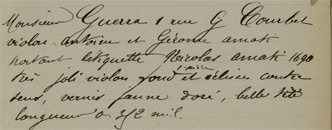

Workshop artisans described remarkable instruments they repaired or assessed in this listing (n° inv. E.981.8.28).

- 1 - Alphabetical index

-

« G » : Alphabetical listing per owner name

- 2 - Instrument description

-

« Monsieur Guerra, 1 rue G. Courbet / violon

Antoine et Gerome Amati / portant étiquette

"Monsieur Guerra, 1 rue G. Courbet / violin Antoine and Gerome Amati / bearing label Nicolas Amati 1690 / very nice 1-piece violin back with splints against the wood-grain, golden yellow varnish, nice head / length o[?] 312 mil."

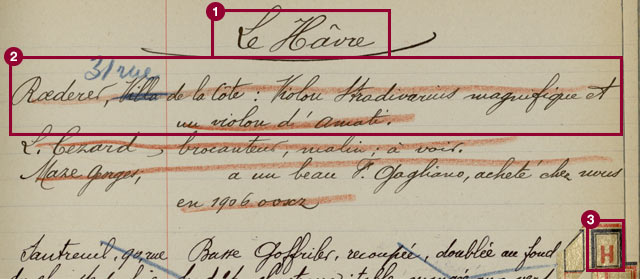

Finding instrument owners (written in Albert Caressa’s day?)

This listing (n° inv. E.981.8.33) records instrument descriptions as well as owners name and address. It may have been a list of potential sellers.

- 1 - City

-

« Le Hâvre »

- 2 - Owner name and instrument description

-

« Roederer,

villa31 rue de la Côte : violon Stradivarius magnifique et / un violon d’Amati »

“Roederer,villa31 rue de la Côte: magnificent Stradivarius violin and / an Amati violin”

- 3 - Alphabetical index

-

« H » : Alphabetical listing per owner address